")

The OPSRP Pension Program is a great benefit for Oregon employees, but their statements tend to be a little hard to understand. We regularly work with people who are counting on the program to fund their retirement, but they don’t understand how it works alongside their other retirement planning tools.

Every Oregon Public Service Retirement Program (OPSRP) member receives an annual statement detailing yearly contributions, growth and service credits – but how can you read that statement? And more importantly, how can you use that information to make better retirement planning decisions?

Today, we’re walking you through all the steps to reading your OPSRP annual statement – let’s get started.

Quick note: If you’d prefer to watch a video walkthrough on this topic, you can watch it below.

How to Read Your PERS’ OPSRP Statement

The Oregon Public Service Retirement Program, or OPSRP, is the lifetime pension program available to all public service workers in the state of Oregon.

OPSRP applies to any individuals hired after August 28, 2003. Prior to that, public service workers were enrolled in the Public Employee Retirement System (PERS). If that’s you, check out our previous blog post.

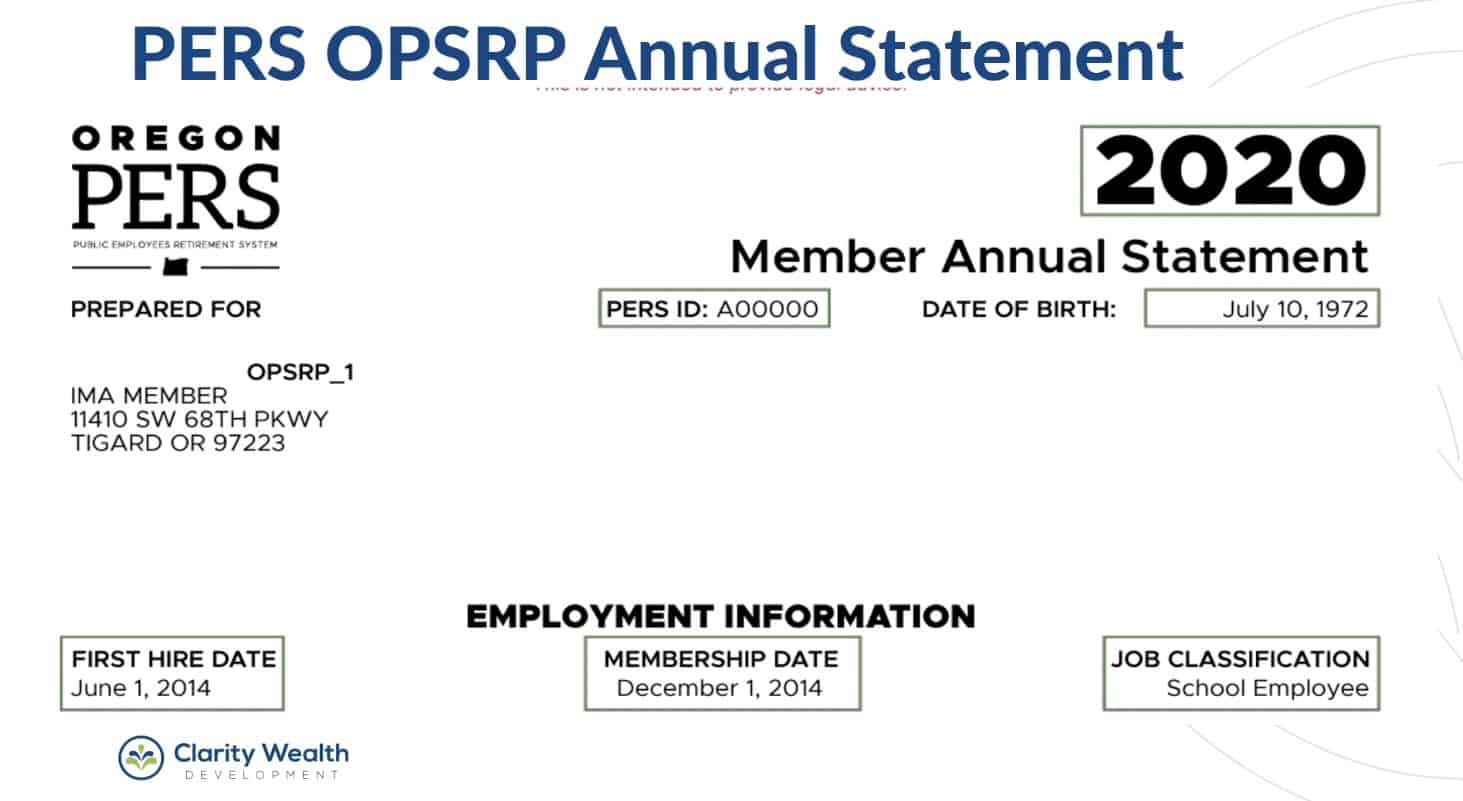

The first section in your OPSRP statement lists all your general information, including your name, the address currently on file, your birth date, and your PERS ID number. It’s imperative that you keep your address up to date so you don’t end up missing any deadlines or important information relating to your pension.

Your PERS ID number is used to identify you in the system. You’ll need this number for all your correspondence, to log in online, and to fill out retirement forms – so keep track of it!

This part of your statement also includes your employment information, including your first hire date and your membership date. While the first hire date tells you when you actually began working, the membership date shows when you started earning retirement credits. Usually, there will be a six month waiting period between these two dates.

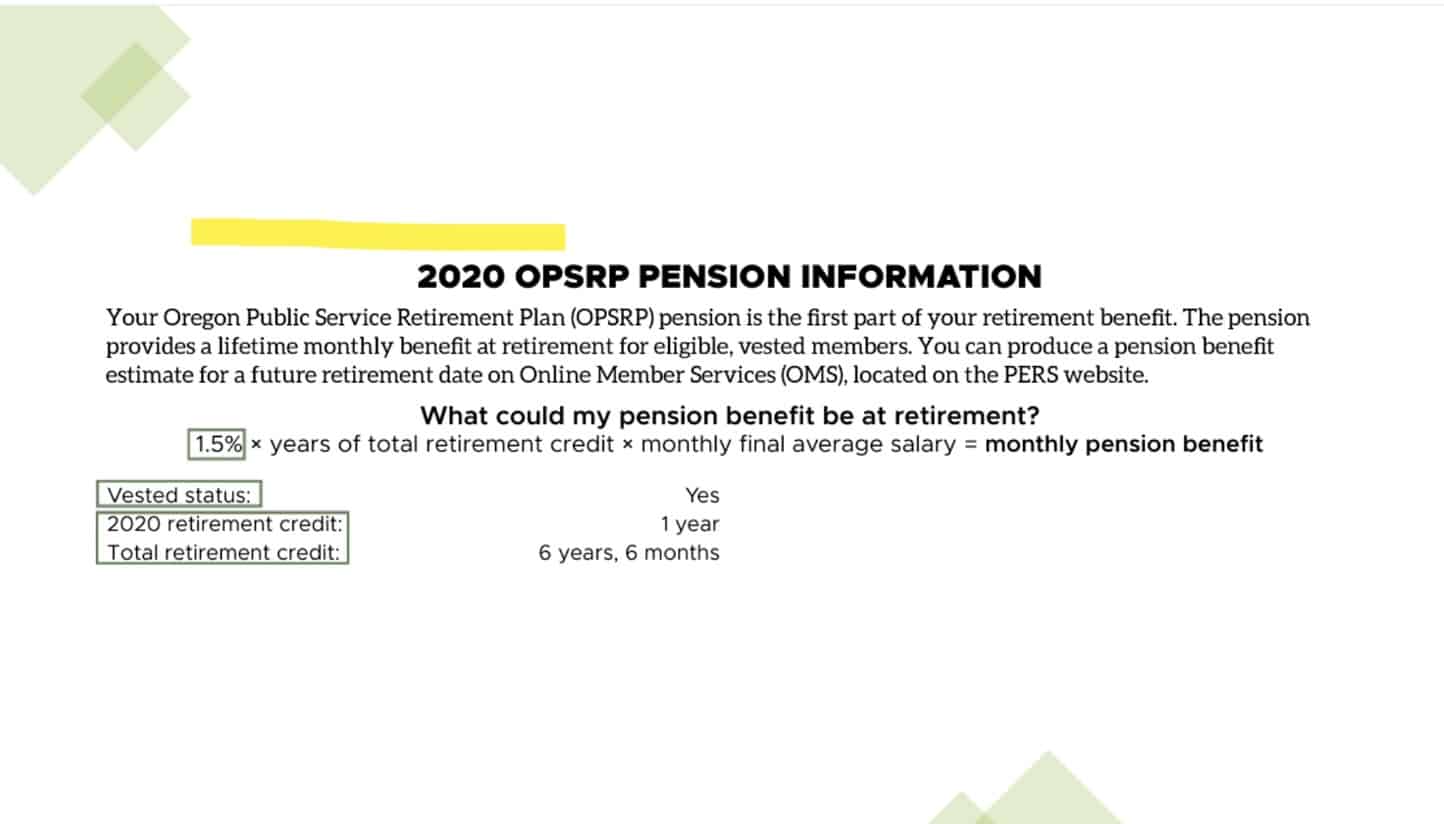

Pension Information

The next section of your statement is titled, “OPSRP Pension Information.” This page details exactly how your retirement benefit amount is calculated. You may notice that the formula takes into account your retirement credits – this is just another term for the amount of years you’ve spent in service.

If you’re quickly approaching retirement (within 6-12 months), you may want to consider requesting a written estimate of your expected monthly benefit. However, keep in mind that you’re only allowed to request this written estimate 1-2 times per year. You are also able to log in to see your estimate as many times as you want, but the online estimate is not as accurate as the written estimate.

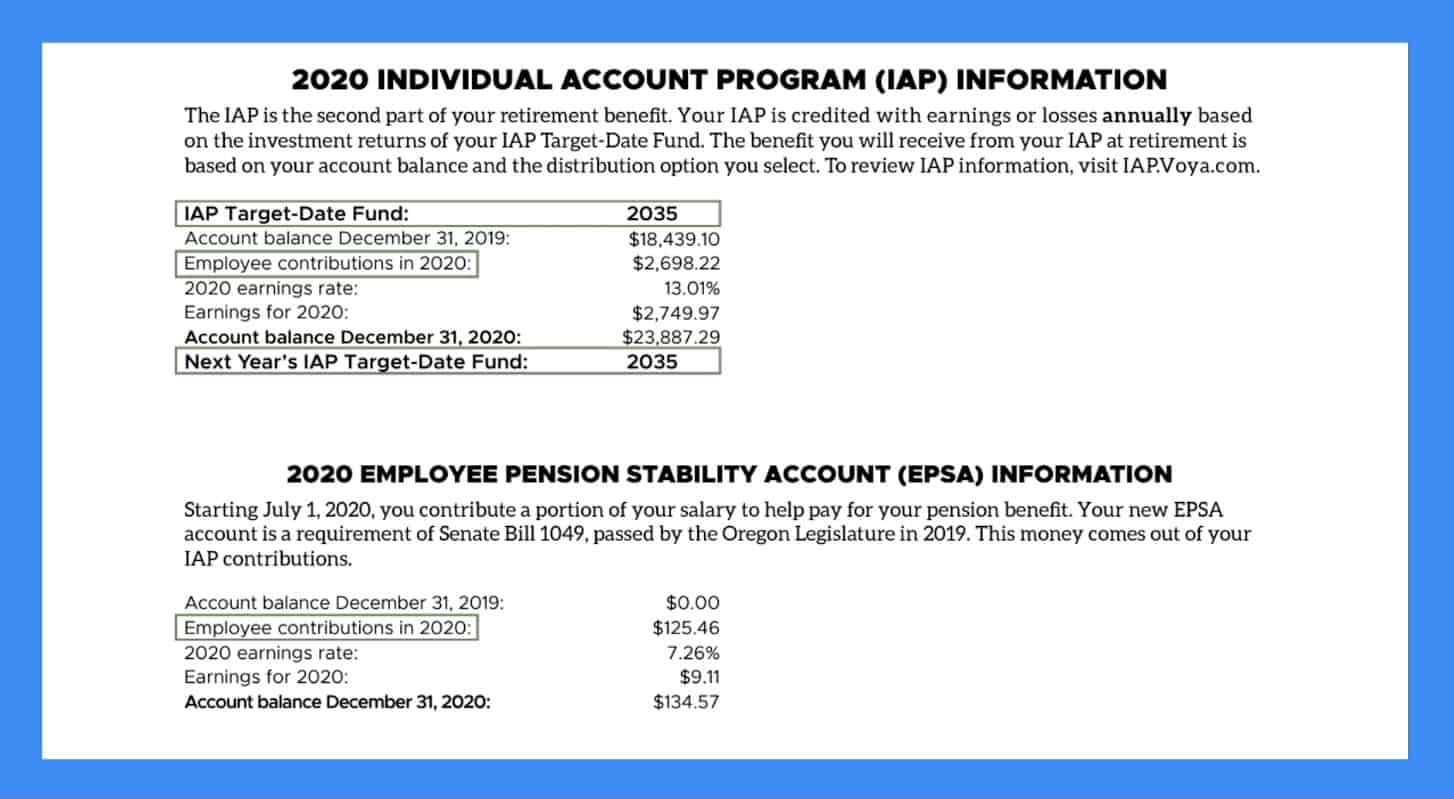

Individual Account Program (IAP) Information

The Individual Account Program, or IAP, shows you the target date fund the OPSRP has selected for your age. For the purposes of this article, the IAP Target-Date Fund is listed as 2035.

Pro Tip: if you want to invest more or less aggressively, you can request this date to be changed through the IAP portal.

The IAP usually consists of 6% of your salary, which may be paid by either you or your employer. When you retire and begin receiving your pension, you’ll have several options as to what you can do with your IAP. You could:

- Rollover your funds into an IRA

- Rollover the amount into an Oregon Savings Growth Plan

- Take distributions

It’s important to note that your IAP must be rolled over or distributed within 15 years from retirement.

Why do people choose Clarity Wealth? Here are three quotes from real clients that break it down for you.

In this section, you can also find the account balance as of December 31 of the previous two years, as well as the total earnings on those investments and how much your contributions were.

To select your distribution option selection when you terminate your service, visit the IAP login website.

Employee Pension Stability Account (EPSA) Information

Lastly, the Employee Pension Stability Account, or EPSA, is a new section of PERS Statements. The funds from your EPSA contributions are used to help pay for your pension benefits.

Passed in 2019, the EPSA collects .75% of total contributions for members making over the monthly income threshold (usually around $3,000). For those under this threshold, you’re likely not paying into the EPSA at all.

How do you know? Well, if you see the EPSA section on your statement, you’re likely paying into the program. If not, you haven’t reached the monthly income threshold and probably aren’t affected.

Plan Your Retirement with Clarity

Want help building a robust retirement plan with advisors who know all the ins and outs of the PERS and OPSRP systems? Visit ClarityWealthDevelopment.com to schedule a complimentary consultation today!